The marble floors and mahogany desks of traditional banking are increasingly sharing space with a new kind of employee one that never sleeps, never takes vacation, and processes millions of data points simultaneously. Throughout 2025 and accelerating into 2026, the global financial services industry has crossed a critical threshold. The conversation is no longer about whether banks should experiment with generative artificial intelligence. It is about how aggressively they can deploy deep AI agents to automate complex reasoning, regulatory compliance, and even client-facing advisory services .

This transformation, widely termed the “Agentic Era,” represents a fundamental departure from the chatbots and robotic process automation of the past decade. Today’s AI agents do not simply wait for prompts; they initiate action, collaborate with other digital entities, and make judgment calls within pre-defined risk parameters. Institutions ranging from BNY and Goldman Sachs to Lloyds Banking Group and Bendigo Bank are now moving from isolated pilot programs to enterprise-wide operational models involving thousands of autonomous agents . This article examines the technological architecture driving this shift, the specific use cases transforming front, middle, and back-office functions, the governance frameworks required to satisfy regulators, and the strategic implications for global systemically important banks.

Defining the Deep AI Agent: Beyond Generative Chat

To understand why the current wave of adoption differs from earlier AI initiatives, one must first distinguish between generative AI and agentic AI. Generative AI, represented by large language models such as GPT-4 or Claude, excels at responding to human queries by producing text, summaries, or code. It is reactive. Agentic AI, by contrast, is proactive. It operates with a goal-oriented framework: assessing an objective, breaking it into subtasks, accessing necessary tools and data sources, executing actions, and adapting its approach based on intermediate outcomes .

A deep AI agent in banking is therefore not merely a sophisticated search engine. It is an entity capable of orchestrating workflows across disparate legacy systems, validating transactions against compliance rules, and even communicating findings to human colleagues via collaboration platforms like Microsoft Teams or Slack. At BNY, for example, certain digital employees now possess their own system credentials, email addresses, and communication access. They function as full participants in the operational fabric of the institution .

This distinction carries profound implications. Traditional automation whether mainframe code or robotic process automation executes deterministic, rule-based tasks. If the rule changes, a human must rewrite the script. Deep AI agents, however, operate within probabilistic environments. They encounter novel situations, weigh alternatives, and select actions based on training and fine-tuning. This capability unlocks efficiency in areas where rigid rules are insufficient, such as interpreting nuanced legal contracts or detecting emergent fraud patterns. However, it also introduces risks related to transparency, bias, and auditability, forcing banks to develop entirely new governance disciplines .

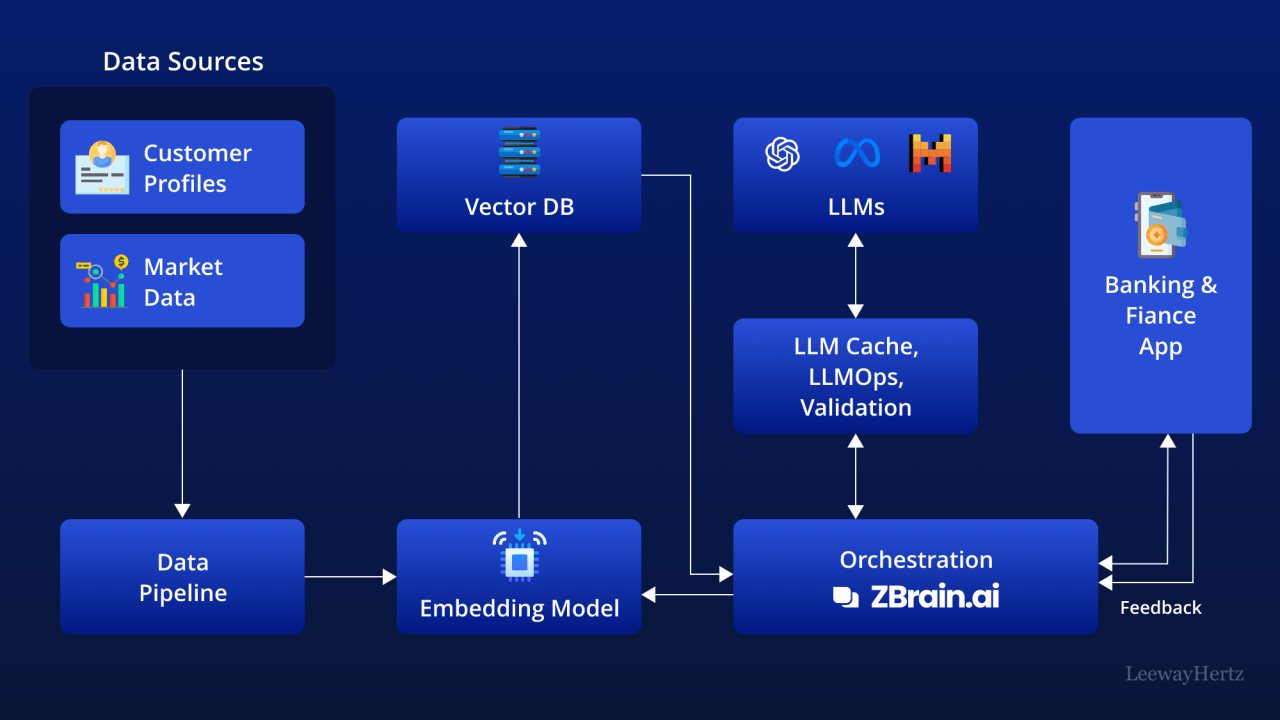

The Architectural Blueprint: Multi-Model, Multi-Cloud, and Explainable

The successful deployment of agentic AI at scale requires an architecture that would have been unimaginable even three years ago. Early generative AI experiments often involved a single large language model accessed via application programming interface. Institutions would feed the model a prompt, receive a response, and hope for accuracy. Production-ready agentic systems, by contrast, depend on sophisticated orchestration layers that manage multiple models, multiple data sources, and rigorous oversight mechanisms.

BNY’s Eliza 2.0 platform offers a leading example of this architectural evolution. Rather than committing to a single vendor, BNY engineered Eliza to be model-agnostic. Depending on the specific task, an agent might invoke OpenAI’s GPT-4 for complex logical deduction, Google Cloud’s Gemini Enterprise for multimodal research synthesis involving both text and numerical data, or a specialized Llama-derivative model for legacy code remediation. This “menu of models” approach prevents vendor lock-in while optimizing performance and cost .

The underlying infrastructure supporting such platforms has itself become a competitive battleground for technology providers. Nvidia solidified its position not merely as a chip supplier but as a critical infrastructure partner, with BNY becoming the first major bank to deploy an Nvidia DGX SuperPOD featuring H100 systems for on-premises training and inference. Microsoft Azure provides the integration fabric connecting Eliza to the Microsoft 365 ecosystem, while Google Cloud contributes deep research capabilities .

Yet hardware and model diversity alone do not constitute an enterprise-grade solution. Perhaps the most significant architectural breakthrough has been the integration of Explainable AI (XAI) frameworks into the agentic pipeline. In regulated financial environments, a model that produces accurate outputs without auditable reasoning is effectively unusable. Regulators and internal compliance officers must understand why an agent reached a particular decision whether denying a trade, flagging a suspicious transaction, or adjusting a credit limit.

BNY addressed this requirement by mandating that every agentic model pass a rigorous Model-Risk Review before deployment. Each model generates detailed “model cards” and feature importance charts that document the factors influencing its outputs. This transparency enables auditors to trace the lineage of decisions and verify that agents are operating within approved parameters . Similarly, platforms such as DSW AgenticAI emphasize audit-first governance, unifying data pipelines, AI models, and GenAI agents within a single compliance-ready framework .

Strategic Deployment Pathways: Smart Overlay, Native Design, and Process Redemption

Deloitte’s comprehensive analysis of banking AI adoption identifies three distinct pathways through which institutions are integrating agentic capabilities. Each pathway carries different cost structures, risk profiles, and time-to-value horizons .

A. Smart Overlay. The most immediately accessible approach involves wrapping existing systems with an intelligent agentic layer. Rather than rebuilding core banking platforms many of which still run on COBOL banks deploy AI agents that interact with these systems via application programming interfaces. This conversational layer can execute standard operating procedures with consistency and compliance. For institutions with substantial legacy investments, the smart overlay offers rapid productivity gains without massive capital expenditure .

B. Native Design. In scenarios where legacy constraints prove insurmountable, banks are pursuing native agentic design. This involves constructing entirely new, autonomous applications for specific functions, often utilizing microservices architecture. These purpose-built agentic systems can be introduced gradually, coexisting with legacy environments while eventually supplanting them. Microsoft’s AutoGen framework and Nvidia’s NeMo services exemplify the platform-level enablers facilitating this approach .

C. Process Redesign. The most ambitious pathway involves fundamentally reimagining workflows to maximize agentic potential. Rather than asking how AI can accelerate an existing process, banks adopting process redesign ask how the process would be structured if autonomous agents were the primary executors rather than human workers. This approach yields the greatest long-term transformation but requires substantial change management and tolerance for implementation risk .

Most large institutions are pursuing a hybrid strategy, applying different pathways to different functional domains based on urgency, complexity, and strategic importance.

Transforming the Front Office: From Transaction Handling to Relationship Augmentation

Customer-facing banking has historically been characterized by a tension between efficiency and personalization. Automated telephone menus and basic chatbots improved transaction speed but often frustrated customers seeking nuanced advice. Deep AI agents are beginning to resolve this tension by assuming responsibility for routine inquiries while simultaneously empowering human relationship managers with unprecedented analytical horsepower.

Lloyds Banking Group, serving over 21 million mobile app customers, articulated a vision in which agentic AI enables “hyper-personalized, always-on services.” Rather than requiring customers to navigate menus and input repetitive information, an intelligent agent embedded in the banking application understands the customer’s financial footprint, anticipates needs, and executes simple actions such as form completion or payment scheduling .

Simultaneously, these agents serve as force multipliers for frontline staff. Relationship managers preparing for client meetings traditionally spent hours gathering data from disparate systems, compiling account histories, and researching market conditions. Agentic tools now consolidate this information, generate preliminary insights, and draft talking points freeing human experts to focus on strategic advisory conversations and emotional intelligence .

Goldman Sachs is pursuing similar objectives through its collaboration with Anthropic. After six months of co-development utilizing Anthropic’s Claude model, the investment bank is preparing agentic tools for trade accounting and client onboarding. These tools automate document-intensive compliance workflows, accelerating response times and reducing manual errors. Goldman emphasizes that the immediate objective is enhanced client experience rather than cost reduction, although reduced reliance on third-party operations providers remains a plausible long-term outcome .

Revolutionizing the Middle Office: Risk, Compliance, and Credit

While front-office applications attract visible attention, the most profound transformations may be occurring in banking’s middle office, where risk management, compliance, and credit analysis intersect. These functions involve processing vast quantities of structured and unstructured data, applying complex regulatory frameworks, and making high-stakes decisions under time pressure precisely the environment where agentic AI excels.

Anti-Money Laundering exemplifies the potential. Traditional AML systems generate enormous volumes of alerts, the vast majority of which prove false upon human investigation. Analysts spend hours or days reviewing transaction patterns, customer histories, and external data sources, only to dismiss most cases. A multi-agent AML architecture might deploy specialized agents for distinct investigative tasks: Agent A reviews monitoring system alerts and identifies specific rules triggered; Agent B analyzes current and historical transaction records; Agent C synthesizes findings and drafts a suspicious activity report. Human investigators supervise the process, verify conclusions, and submit reports to regulators. This orchestrated approach compresses investigation timelines while potentially uncovering illicit patterns that human analysts might miss .

Credit underwriting is undergoing parallel transformation. Auquan, a specialized provider of agentic AI for institutional credit markets, developed a Credit Agent that reads borrower financial statements and data room documents, extracts key fields and covenant details into structured formats, accesses subscription-based and public information sources, applies the institution’s internal risk frameworks, and drafts investment committee memos conforming to firm-specific templates. Large institutional investors using this system have reduced review times from days to hours across substantial credit portfolios, enabling them to evaluate more opportunities without expanding analyst headcount .

The strategic significance of this shift extends beyond operational efficiency. Auquan CEO Chandini Jain observed that the competitive advantage in finance is migrating from the quantity of analysts to the quality of encoded judgment. Institutions that successfully codify their underwriting philosophy, risk tolerance, and proprietary data into agentic systems can deploy that judgment at software speed and marginal cost approaching zero. This dynamic advantages incumbents with rich historical data while challenging competitors reliant solely on generic intelligence .

Reimagining the Back Office: Digital Employees and Autonomous Operations

BNY’s January 2026 announcement that it had deployed over 20,000 “Empowered Builders” and more than 130 specialized “Digital Employees” represents the most dramatic public demonstration of back-office agentic transformation . These digital employees are not metaphorical constructs; they possess authenticated system access, appear in organizational directories, and execute workflows spanning multiple applications and approval stages.

The practical impact manifests in measurable efficiency gains. BNY reported approximately 5 percent reduction in unit costs for core custody trades a significant margin in the high-volume, low-margin asset servicing business. Contract Review Assistant agents benchmark thousands of negotiated agreements against evolving global regulations, performing work that previously required coordination among legal, compliance, and business teams .

Citi’s enhancements to its Stylus Workspaces platform follow a comparable trajectory. By integrating agentic features that connect internal datasets, productivity tools, and structured reasoning, Citi enables employees to complete research-intensive tasks with dramatically accelerated velocity .

These back-office deployments also illuminate the evolving human-machine collaboration model. Earlier automation waves replaced manual data entry; current agentic systems perform tasks previously requiring human judgment and cross-departmental coordination. This progression creates new supervisory responsibilities. Human managers increasingly oversee portfolios of digital employees, monitoring their decisions, resolving exceptions, and refining their operating parameters. The development of management frameworks suited to this hybrid workforce constitutes an urgent organizational priority .

Governance, Risk, and the Regulatory Imperative

The expansion of agentic autonomy in banking inevitably intensifies scrutiny from risk officers and regulators. Each autonomous decision carries potential for error, bias, or compliance failure. Moreover, agentic systems operating across multiple legacy platforms may inadvertently create new connectivity vulnerabilities, expanding the attack surface available to malicious actors .

Forward-looking institutions are responding by embedding governance directly into agentic architecture rather than treating compliance as an afterthought. BNY’s insistence on transparent, auditable agent behavior reflects recognition that regulatory acceptance hinges on explainability. Google Cloud’s Gemini Enterprise incorporates strengthened security controls and responsible-AI features specifically designed to satisfy financial services compliance requirements .

Lloyds Banking Group established a dedicated Responsible AI team charged with testing every agentic deployment against rigorous guardrails, scenario plans, and escalation protocols. The group emphasizes that responsible innovation is not a constraint on progress but rather the foundation for sustainable scaling .

Despite these efforts, industry-wide governance gaps persist. A Collibra report cited by Banking Dive found that fewer than half of companies have established comprehensive AI governance policies. Employee training around compliance and responsible use lags behind adoption ambitions . This disconnect suggests that some institutions may be deploying agentic capabilities faster than their control environments can accommodate a dynamic that historically precedes regulatory intervention.

The Vendor Ecosystem and the Build-vs-Buy Calculus

As agentic AI moves from experimental to operational, banks face complex decisions regarding technology sourcing. The landscape now includes multiple categories of providers, each offering distinct value propositions.

Hyperscale cloud providers Google, Microsoft, and Amazon offer foundational models and development platforms. Google’s Agentspace, Amazon Bedrock’s multi-agent collaboration features, and Microsoft’s Azure AI services provide building blocks for institutions with strong internal engineering capabilities .

Specialized AI startups offer domain-specific solutions embedding deep vertical expertise. Anthropic collaborates directly with Goldman Sachs on customized agent development . Auquan targets institutional credit with pre-configured underwriting and monitoring agents . DSW AgenticAI provides an enterprise platform with integrated DataOps, development studio, and workflow orchestration tailored to banking and insurance compliance requirements .

Systems integrators and consultants assist with the complex work of connecting agentic systems to legacy environments, reengineering processes, and upskilling workforces.

No single vendor currently offers a complete, end-to-end agentic suite covering all banking use cases. Institutions must therefore architect multi-vendor strategies, balancing the flexibility of best-of-breed components against the complexity of integration and governance .

Workforce Implications: Empowerment, Displacement, and New Capabilities

The agentic shift inevitably raises questions about employment. Banking has historically been a stable, career-oriented industry, and the prospect of digital employees assuming tasks previously performed by university-educated professionals generates understandable anxiety.

Available evidence suggests a more nuanced outcome than simple displacement. BNY’s “Empowered Builders” program trained thousands of existing employees to construct and maintain custom agents, democratizing AI development skills across the organization rather than concentrating them within a specialized technology cadre . Lloyds launched a Group-wide AI Academy offering practical, accessible learning pathways, from mandatory responsible AI training to role-specific upskilling .

These initiatives reflect recognition that agentic AI does not eliminate the need for human judgment but elevates its importance. As agents handle routine verification, reconciliation, and documentation, human workers increasingly focus on handling exceptions, resolving ambiguous situations, refining agentic frameworks, and engaging with clients on complex advisory matters. The required skill profile shifts from procedural accuracy to critical thinking, communication, and continuous learning.

Nevertheless, certain job categories face structural pressure. Roles centered on high-volume document review, manual data reconciliation, and routine compliance checking will likely contract. Banks have so far been cautious about linking agentic deployment to workforce reduction targets, perhaps mindful of stakeholder and regulatory sensitivities. Yet the economic logic of automation suggests that efficiency gains will eventually flow to the bottom line through some combination of reduced hiring, attrition management, and organizational restructuring .

The Horizon: Proactive Agents and Autonomous Remediation

Current agentic deployments, while advanced, remain predominantly reactive. Agents receive assignments, execute defined workflows, and report outcomes. The next frontier involves truly proactive agents that anticipate needs and initiate remediation before problems materialize.

BNY is actively developing Predictive Trade Analytics agents capable not merely of identifying settlement risks but autonomously initiating corrective actions to prevent trade failures. This transition from “detect and report” to “anticipate and act” represents the ultimate test of agentic autonomy in finance. If successful, it will reduce operational losses and enhance market stability. It will also intensify debates regarding accountability when autonomous systems make errors .

Client-facing autonomous agents constitute another emerging frontier. BNY is reportedly exploring “Client Co-pilots” that would grant institutional clients direct access to agentic research and analysis tools. This application raises complex challenges regarding data privacy and multi-tenant security architecture. Agents must not inadvertently share proprietary insights across different client accounts, and clients must clearly understand whether they are interacting with a human or an algorithm .

Conclusion: The New Operating System of Finance

The deployment of deep AI agents across banking is neither incremental improvement nor speculative experiment. It represents a foundational shift in how financial institutions process information, manage risk, and serve clients. BNY’s characterization of agentic AI as the “operating system of the bank” captures the essence of this transformation .

Institutions that successfully navigate this shift will achieve durable competitive advantages: faster decision cycles, more consistent compliance, lower operational costs, and enhanced capacity for personalized service. Those that lag face gradual obsolescence as the industry’s efficiency frontier advances beyond their reach.

Yet the agentic era also carries responsibilities that the industry is still learning to fulfill. Transparency, fairness, accountability, and resilience cannot be afterthoughts retrofitted to completed deployments. They must be engineered into agentic systems from inception, supported by governance frameworks as robust as those governing human decision-makers.

The year 2026 will likely be remembered as the point at which agentic AI moved definitively from pilot projects to production systems at scale across global banking . The question no longer is whether this technology will transform finance. The question is which institutions will lead the transformation, and whether they will do so in a manner worthy of the trust placed in them.

{kind=link}