The rumble of a V8 engine and the scent of gasoline have long been the defining sensorial signatures of the automobile. For over a century, the industry’s competitive moats were dug with mechanical wrenches, forged from stamped steel, and defended by patents on turbochargers and transmissions. However, under the hoods of the vehicles slated for release in 2026 and beyond, the battlefield has shifted dramatically. It is no longer about horsepower; it is about floating-point operations per second (FLOPS), over-the-air (OTA) update cadence, and the seamless integration of silicon and code .

This is the era of the Software-Defined Vehicle (SDV), and a brutal, high-stakes war is currently erupting across the global automotive landscape. On one side, traditional European and American manufacturing behemoths weighed down by legacy organizational structures are scrambling to shed their hardware-first DNA. On the other side, agile Chinese electric vehicle (EV) makers and West Coast tech giants are capitalizing on their digital-native speed. This conflict, characterized by shattered monopolies on intellectual property, massive capital infusions into middleware startups, and a frantic race to secure code, is the defining business narrative of the modern auto industry .

The Collapse of the ‘Built-From-Scratch’ Dogma

For decades, the mantra of the incumbent automaker was vertical integration. If it went into the car, the logic went, the OEM must own it. This philosophy reached its peak (and subsequent breaking point) with ventures like Volkswagen Group’s Cariad. Launched with the ambition to be the “SAP of the automotive world,” Cariad was supposed to unify the software stacks of Audi, Porsche, and VW under a single, powerful proprietary roof. Instead, it became a cautionary tale etched into the balance sheets of the entire group .

The failure of this strategy was not due to a lack of funding or talent, but rather a fundamental mismatch in corporate anthropology. Building a braking system that lasts 200,000 miles follows a linear, waterfall development model. Building an operating system that processes sensor fusion for Level 3 autonomy requires agile sprints, continuous integration, and a tolerance for iterative failure that legacy automakers are not structurally designed to handle. As noted by Gartner’s research, proprietary software strategies in the automotive sector have largely failed because they are “too slow and too expensive” .

The repercussions of this realization have sent shockwaves through the C-suites of Europe. Stellantis’ shelving of its “AutoDrive” L3 program and Audi’s high-profile software-related recalls (such as the rearview camera glitch affecting U.S. models) serve as stark reminders that even minor coding errors can erode consumer trust faster than any mechanical failure ever could . The industry has thus reached a critical inflection point: the admission that no single automaker can or should write every line of code in a modern vehicle. This has triggered an unprecedented pivot from “defend and control” to “acquire and integrate.”

The Rise of the ‘Zonal’ Brain and the Middleware Gold Rush

To understand why the software battles are intensifying, one must look at the physical transformation of the vehicle’s nervous system. Traditional cars operate on a distributed architecture, featuring dozens of Electronic Control Units (ECUs), each responsible for a single function (e.g., the window ECU, the seat ECU). This model is collapsing under its own weight due to wiring harness complexity and computational redundancy .

The industry is rapidly migrating toward Zonal E/E Architectures. Instead of 100 separate boxes, the vehicle is divided into four to six physical zones (front left, front right, etc.), each managed by a high-performance central computer. Tesla pioneered this, and legacy brands are now sprinting to catch up . While this shift cuts wiring weight by up to 30% and reduces assembly costs, it transfers immense complexity to the software layer.

This is where the concept of Middleware has transitioned from a niche IT term to a boardroom-level strategic asset. Middleware is the “digital glue” that allows the applications (ADAS, infotainment) to speak to the hardware (NVIDIA chips, Qualcomm SoCs) without needing to be rewritten for every specific model. The recent acquisition of TTTech Auto by NXP Semiconductors for $625 million was not a minor supply chain move; it was a declaration that owning the safety-certified middleware pipeline is now as critical as owning the fab .

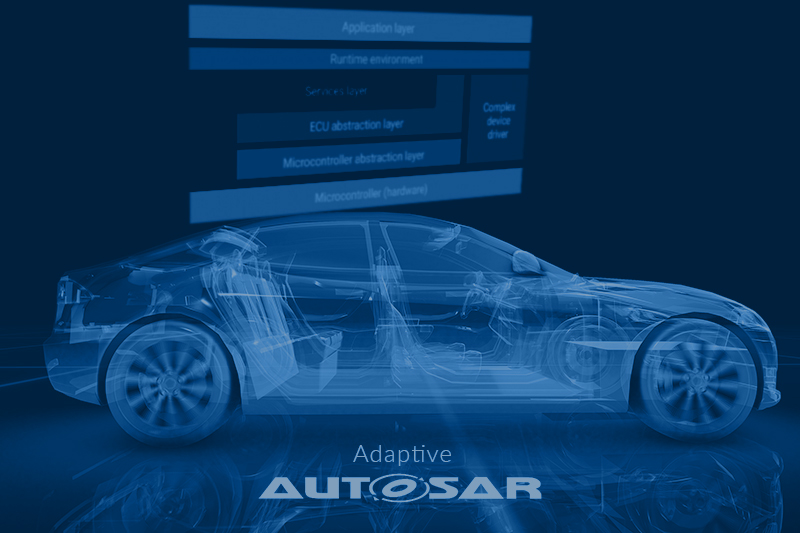

However, this migration is fraught with friction. The lack of standardized APIs across the industry forces Tier-1 suppliers to port the same functions to multiple proprietary stacks a wasteful exercise that inflates validation expenses. While consortia like AUTOSAR (Classic and Adaptive) and SOAFEE attempt to harmonize these frameworks, divergent brand strategies, particularly among premium European OEMs, stall convergence .

The Geopolitics of Code: Asia’s Velocity vs. Europe’s Compliance

The competitive landscape of automotive software is no longer just corporate; it is distinctly geographical. According to market analysis from late 2025 and early 2026, Asia-Pacific currently commands the largest regional share of the software market, projected to grow at a staggering CAGR of over 11% .

China’s Advantage: Speed and Ecosystem

Chinese OEMs such as BYD, XPeng, and Zeekr operate under development cycles that are up to 60% faster than their Western counterparts . This velocity is not accidental. It is enabled by an ecosystem approach that foreign competitors are only now beginning to mimic. Rather than isolating themselves, Chinese automakers embedded themselves within vast digital ecosystems (Huawei, Baidu, Tencent, Alibaba) from the very beginning .

This collaboration goes beyond simple supplier relationships. It includes:

-

A. Deep Technology Integration: Full-stack solutions via Huawei Inside (HI) or Horizon Robotics for ADAS chips.

-

B. Platform Sharing: Open architectures like Geely’s SEA or e-platform 3.0, which are licensed to external brands.

-

C. Rapid Feature Iteration: Function updates measured in weeks, not years, driven by real-time user data feedback loops.

This ecosystem approach allows Chinese firms to dominate in Application Software the layer responsible for ADAS features and user experience which currently accounts for nearly half of the market’s revenue .

Europe’s Burden: Compliance and Talent Shortages

Europe maintains a formidable position in the market, but its growth trajectory is pinned by regulatory gravity. While UN Regulation WP.29 and the Cyber Resilience Act are necessary for safety, they act as a tax on speed. A survey of 1,100 automotive developers by QNX revealed that one-third of developers have faced delayed timelines directly due to evolving compliance mandates. Cybersecurity and ISO 21434 compliance alone challenge 47% of development teams .

Furthermore, Europe faces a severe shortage of AUTOSAR-certified developers. This scarcity inflates labor costs and risks schedule slippage. While automakers like BMW are attempting to mitigate this through offshore engineering hubs (such as the BMW TechWorks India joint venture with Tata), the continent is still struggling to balance its rigorous safety heritage with the need for rapid code deployment .

The Developer’s Dilemma: Safety, Security, and the Rust Question

Zooming in from the macro boardrooms to the micro level of the integrated development environment (IDE), the software battles are being fought on actual command lines. The Perforce Automotive Software Development Report for 2025 highlights a significant shift in developer priorities. For the first time in a cycle, software quality has overtaken pure security concerns as the primary headache, with safety returning to the number two slot .

Key Technical Bottlenecks Identified by Developers:

-

A. Functional Safety (ASIL-D): 38% of developers are required to achieve the highest Automotive Safety Integrity Level (ASIL-D). This demands rigorous adherence to coding standards like MISRA, which significantly slows down the velocity of feature deployment .

-

B. Language Politics: Despite hype surrounding “memory-safe” languages, C++ remains the undisputed king (54% usage) , followed by C (44%). Rust has actually seen a 3% decline in year-over-year usage. Developers cite a lack of mature compilers, analyzers, and established coding standards as barriers to adopting Rust for production-critical, safety-certified projects .

-

C. Open Source Skepticism: While most developers use open-source tools, there is a distinct reluctance to contribute back. Resource constraints and fears of hidden vulnerabilities in shared code libraries persist .

This technical debt creates a critical bottleneck. While executives promise “AI-ready” and “app-store-enabled” vehicles, the engineers on the ground are struggling to debug deterministic real-time operating systems (RTOS) and ensure that zone controllers don’t fail silent.

The New Power Brokers: Hyperscalers and Chip Designers

As the line between a consumer electronics device and a vehicle blurs, the balance of power in the supply chain is tilting away from the traditional OEM. The automotive value chain is no longer linear (Supplier → Tier-1 → OEM → Dealer). It has become a networked web.

Chipmakers as Software Vendors

Companies like NVIDIA, Qualcomm, and NXP are no longer just selling silicon; they are selling reference platforms and software development kits. Volkswagen’s recent deepening of ties with Qualcomm is indicative of this shift. VW isn’t just buying modems; it is adopting Qualcomm’s compute stack and Snapdragon Digital Chassis to standardize its fragmented global portfolio . These chipmakers are bundling their hardware with optimized middleware and AI toolchains, effectively bypassing traditional Tier-1 integrators.

Hyperscalers Enter the Garage

Microsoft, Google, and Amazon Web Services (AWS) are aggressively pushing into the vehicle. While Android Automotive and QNX battle for infotainment supremacy, the back-end cloud infrastructure that processes the terabytes of data generated by autonomous fleets is dominated by the hyperscalers. This allows them to capture recurring revenue streams long after the vehicle is sold, shifting the industry from a one-time transaction model to a subscription-based, function-on-demand model .

Monetization and the Aftermarket Recoil

With great software power comes great monetization ambition. Automakers, facing thin margins on hardware (exacerbated by expensive battery costs), view software as the high-margin goldmine they have been searching for. Subscription services for heated seats, enhanced autonomous driving packages, and dynamic battery range extensions are becoming standard revenue experiments .

However, this has created a cultural recoil among driving enthusiasts. As noted in automotive aftermarket analyses, there is a growing sentiment that while “software is the new horsepower,” hardware still wins hearts .

Consumers are growing weary of “beta testing” expensive hardware through OTA updates. The novelty of receiving a new ringtone for the car is wearing off, replaced by anxiety over system crashes and subscription fatigue. This presents a unique opportunity for the aftermarket sector. As OEMs focus on abstract code, the demand for tactile, reliable hardware upgrades performance brakes, superior suspension damping, lightweight wheels is rising. Enthusiasts are seeking the “antidote to modern bloat,” preferring vehicles that feel mechanically predictable over those that require a terms-of-service agreement to start the engine .

The Regulatory Hammer and the Recall Landscape

It is impossible to discuss the automotive software landscape without addressing the elephant in the server room: regulatory compliance as a competitive barrier. The days of shipping flawed code and fixing it later (the “move fast and break things” mantra) are incompatible with ISO 26262.

The regulatory environment has bifurcated the market. In North America, the Inflation Reduction Act (IRA) is driving demand for battery-management software and telematics . In Europe, WP.29 R156 mandates that OEMs demonstrate secure and capable OTA update processes. Non-compliance doesn’t just result in a fine; it results in a stop-sale.

The Audi rearview camera recall serves as a perfect parable. It was not a complex autonomous driving failure; it was a relatively simple display glitch. Yet, it became a “safety story, a compliance story, and a trust story all at once” . This proves that in the SDV era, software reliability has become synonymous with brand prestige.

The Road Ahead: 2026 to 2035

Forecasting the trajectory of the automotive software market reveals a compound annual growth rate ranging from 9.33% to 14.3%, with valuations expected to hit anywhere from $32 billion to over $90 billion by the early 2030s .

Several distinct trends will define the next phase of these battles:

-

Generative AI in the Loop: By 2026, generative AI is moving beyond the concept phase. KPIT Technologies and others are embedding proprietary GenAI into the vehicle development lifecycle. This will accelerate the creation of virtual validation environments and personalized in-cabin assistants. However, new standards like ISO/PAS 8800 will be crucial to certifying AI that makes safety-critical decisions .

-

Consolidation of the Middle Tier: There are too many middleware vendors chasing too few standardized platforms. Expect aggressive M&A activity as automakers look to acquire boutique safety-software houses to secure their supply chains.

-

The ‘White Label’ Software Supplier: Just as Magna makes cars for Mercedes, we will see the rise of pure-play software suppliers who provide the entire digital cockpit or ADAS stack as a black-box solution to OEMs who have given up on proprietary development .

-

The Indian Engineering Surge: With talent shortages crippling Europe, the software engineering capabilities in India are becoming a critical export. Joint ventures like BMW-TechWorks will be replicated across the industry as the “German Engineering, Indian Coding” hybrid becomes a necessity, not a choice .

Conclusion

The automotive software battles that began in the early 2020s are no longer preliminary skirmishes; they are a full-scale war of attrition. The “Great Automotive Mindshare War” of 2026 is defined by a single, unifying truth: the car is no longer a product, but a platform.

For legacy European giants, victory requires a painful abdication of the “not-invented-here” syndrome and an acceptance that the most efficient path to the SDV future is paved by partners in Silicon Valley and Shenzhen . For Chinese innovators, the challenge lies in translating domestic speed into global scale while navigating geopolitical trade barriers.

For the consumer, the short term may bring growing pains glitchy infotainment systems, subscription paywalls, and the uncanny feeling of a car that updates itself overnight. Yet, the long-term trajectory points toward vehicles that are safer, more efficient, and continuously improving.

Ultimately, the winner of the automotive software battle will not be the company that writes the most lines of code. It will be the company that best orchestrates the complex interplay between brilliant silicon, bulletproof real-time operating systems, and the human desire for a driving experience that feels both magical and utterly dependable. The arms race is on, and the code is the ammunition.

{kind=link}